Filed under: Combs & Company, Feature Friday, HR, Racism | Tags: Combs & Company, Feature Friday, HR, Mike Veny, Racism in the Workplace, SHRM

Click Here for the original post on The SHRM Blog!

As a mental health speaker, much of my work is focused on supporting HR leaders around mental health initiatives. This usually involves addressing the mental health stigma. I’ve learned having uncomfortable and awkward conversations is the critical key to transforming this stigma.

We don’t usually like to have these types of conversations. But they help us reach a place of understanding.

The same is true for navigating racism.

We will only make real and lasting progress in this area when we focus on empathizing with people who have different perspectives than us. It’s important to understand that we’re never going to fully understand someone who is living in a different set of shoes. But we can do our best to have empathy so we can reach a place of connecting better. And ultimately be able to get more done together.

What you need to keep in mind as an HR leader

- Many people of color are angry, sad and scared right now. Those are difficult emotions that make it hard to focus, communicate and respond to everyday situations. They often stem from not feeling listened to or feeling a lack of control over what’s happening in life.

- Company words right now need to be more authentic than ever and backed up by action. Your initiative cannot be about meeting the status quo to avoid being a victim of the “cancel culture”.

- Diversity and Inclusion training needs to be an ongoing, regular part of your work. This will ultimately lead to increased productivity and profitability. You may need to use this angle when talking with your C-level executives about your initiative.

- Learn to ask the right questions and then listen. Here are some examples:

○ “What do you see happening that I don’t see?”

○ “How do you think you are perceived by the leaders in the company?”

○ “What do you feel we need to be doing that we’re not doing?”

○ Or simply say, “Help me understand.”

Creating effective messaging

Right now, people want to hear what your company stands for. Let them know that you don’t support racism. Share your policies and what the company is doing to prevent it. Then, BE LOUD with your actions showing the follow-through. The more public you are, the more trust you will build if you follow it up with action. Don’t get caught saying one thing and doing another!

Please understand that it’s important to embrace not getting it right. No matter how much you “perfect” your message, there will be people who think you’re saying it wrong or not saying enough. We’re not going to get it just right. But the important thing is making sure that we do our best to understand and empathize with others’ perspectives. It’s really that simple.

__________________________________________________________________

Mental health speaker and best-selling author Mike Veny delivers engaging presentations with raw energy and a fresh perspective on Diversity and Inclusion. He shares how he went from struggling with mental health challenges to being a thought leader that travels the globe telling his story to help transform stigma.

He is a highly sought-after keynote speaker, corporate drumming event facilitator, author, and luggage enthusiast. Seriously, you’d completely get it if you did all the traveling he did!

Mike is the author of the book Transforming Stigma: How to Become a Mental Wellness Superhero & The Transforming Stigma Workbook. As a 2017 PM360 ELITE Award Winner, he is recognized as one of the 100 most influential people in the healthcare industry for his work as a patient advocate.

Filed under: Combs & Company, Covid-19, Disaster Relief, HR, Insurance 101 | Tags: Chelsea Whalley, Covid-19, Furloughed Employees, Human Resources, J Donovan Financial

Strategizing on how to bring some furloughed employees back? Check out this great video from colleague, Chelsea Whalley of J Donovan Financial.

1. Create a staffing plan that revolves around the needs of the COMPANY first. Ask yourself where you anticipate being busy and where you may be slower. Create a plan accordingly.

2. Choose which staff return based on unique skill sets needed, overall job performance, seniority/tenure, or their willingness to do jobs outside of their normal scope.

3. DO NOT discriminate based on age, perceived disabilities, or by retaliating for taking paid sick leave.

Make sure to DOCUMENT your process ahead of time and COMMUNICATE to your staff your plan to avoid unnecessary stress for everyone.

*REMEMBER TO ALWAYS CONSULT YOUR ATTORNEY OR HUMAN RESOURCES VENDOR FOR ADVICE* If you need these types of vendors, we can refer you to them.

Filed under: Combs & Company, Covid-19, Giving Back, HR, Mental Health, Reopen Strategy | Tags: Covid-19, Employers, Mental Health, Mental Wellness, Mike Veny, Reopen Strategy

As talks of reopening start happening and, as an employer, you begin to make a strategy for what this will look like, Mental Wellness should be in the forefront of your checklist.

As talks of reopening start happening and, as an employer, you begin to make a strategy for what this will look like, Mental Wellness should be in the forefront of your checklist.

Mike Veny, Mental health speaker, drummer and best-selling author shares a powerful checklist on how to support your employees during this time. This list includes:

1. Change the way you view everyone.

2. Understand there are different levels of anxiety.

3. Remember everyone has a unique home situation.

CLICK HERE to download the entire list and advice on how to implement!

_________________

213-458-8369

mike@mikeveny.com

Filed under: Affordable Care Act, Combs & Company, Combs & Company Blog, HR, Important Notice, Obamacare, Reform, Susan L Combs | Tags: ACA, Combs & Company, Insurance Terms, National Healthcare, Penalties

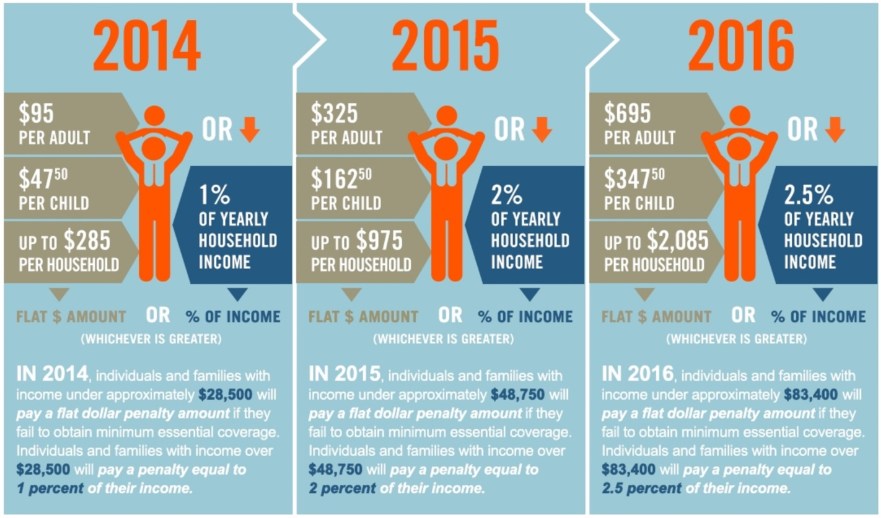

So we are in the home stretch! Three more days to go and then Open Enrollment ends for 2016. From experience, I have learned that many people wait until the last minute to pick a plan and some people just continue to bury their heads in the sand. So for those of you that are wondering, how much it’s going to cost you if you don’t get your act together, take a look at this user friendly graphic that will show you what to expect!

Filed under: Affordable Care Act, Health Insurance, HR, Obamacare, PPACA, Reform | Tags: ACA Auditing Services, Insurance Consulting

Since the start of 2014 we’ve been approached by CPAs, attorneys, and other trusted advisors to assist them with Affordable Care Act (ACA) audits, to determine if their clients will be subject to the “Pay or Play” provision come 2015, and then in 2016 if they have more than 50 Full-Time Equivalent (FTE) employees. I wanted to take this opportunity to introduce our ACA auditing services to you.

Currently I’m one of seven brokers in the New York Metro area with a Patient Protection & Affordable Care Act (PPACA) certification through the National Association of Health Underwriters (NAHU). The certification is key, as I’m trained on all the variables within the ACA law and how it impacts companies of various sizes; plus the continuing education keeps me fully informed as Washington adjusts different provisions of the law.

For 2015, companies that have more than 100 FTE employees will be required to offer health coverage to all employees or they will be subject to a fine. That coverage must include the 10 Essential Benefits, or the company will be subject to a different fine. Combs & Company will perform the ACA audit and produce a report that highlights all provisions with which a company must comply (and the consequences if they don’t). We’ll also devise a look-back measurement the company should use to minimize any potential penalties. We’ll also review any Common Ownership issues, as these are often overlooked areas that can impact companies.

This is not a pitch to replace a company’s current broker. We’re offering this service to support a company’s current setup and because we know the level of expertise we bring to the table is not yet common in the industry. (Nor do most brokers want to assume the liability.) We will work with your client’s current broker to gather as much information as possible and then incorporate them into the audit process.

Our service is offered at a rate of $250/hour. The length of each audit depends on the complexity of your client’s business and health plans. We also have an in-house ERISA Attorney who can provide additional services for a flat fee, should any compliance issues come to light during the ACA audit.

If you’re interested in finding out more or having your client schedule a planning meeting with us, feel free to reach out!

Filed under: Affordable Care Act, Exciting News, Health Insurance, HR, Important Notice, National Healthcare, Obamacare, PPACA, Reform

A question that comes up time and time again with the Affordable Care Act is: “How does the Individual Responsibility (aka Mandate) Penalty work?”

To avoid the penalty you must enroll in a marketplace plan OR have private coverage no later than March 31st, 2014. If you do not, below are a breakdown of the penalties you will face.

- 2014: Greater of $95 per adult and $47.50 per child under age 18 or 1% of household income

- 2015: Greater of $325 per adult and $162.50 per child under age 18 or 2%

- 2016: Greater of $695 per adult and $347.50 per child under age 18 or 2.5% of taxable gross income capped at the average bronze-level insurance premium (60% actuarial) rate for the person’s family.

**The total family penalty is capped at 300% of any annual flat dollar amount for those 18 and over.

**If the penalty applies for less than a full calendar year, the penalty will be 1/12 of the annual amount per month without coverage.

Example:

Let’s look at the O’Brien family of 4 that has 2 children under the age of 18 and the family household income is $100,000 per year.

Just to make the example easier, we are giving everyone names….Meet the O’Brien Family: Mom – Samantha; Father – Mark; Son – Luke; Daughter – Sarah

Upfront we know that the Max Penalty the O’Brien’s’ can be given is: $570 (this is figured by a $95 penalty each for Samantha & Mark since they are the only ones over 18 x 300%), now let’s look at the breakdown if they would hit the Max Penalty….

Remember, it is the GREATER of the below up to the Max Penalty:

Flat dollar amount penalty calculation : $95 (Samantha) + $95 (Mark) + $47.50 (Luke) + $47.50 (Sarah) = $285

Percentage amount penalty calculation: 1% of $100,000 = $1000

Results: Since the Max Penalty the O’Brien family can be given in this example is $570, this will be the penalty they will be responsible for, since the 1% of household income exceeds this amount. This amount will be tacked on when Samantha and Mark’s taxes are calculated at the end of the year, so if they were planning on a nice refund this year, that will be deducted from that refund. Keep in mind that if the O’Brien’s do not pay taxes, as of now, there is no mechanism to collect this penalty.

I had a client that sent me this article and then asked if it was true, that if someone makes $1 more that the family would be paying $9,355 more annually.

I had a client that sent me this article and then asked if it was true, that if someone makes $1 more that the family would be paying $9,355 more annually.

I know there are a lot of confusing articles out there right now and this was written with a shock factor to get you to read the article, and for my client….it worked! He read it, and he contacted me to be his “BS Meter” as he put it.

Here is an example to further explain why this article is saying what it is say:

Ok, so let’s say it is a family of 4.

400% of the federal poverty level is around $95,000 for a family of four in 2014. If they are making $95,000, then with their subsidy aka discount they will get in the Exchange / Marketplace they cannot spend more than 9.5% of $95,000 on healthcare. Which translates to $9025 annually = $752 per month (just as a barometer, most family coverage in NY starts at around $1200 per month for a very watered down plan).

If the person makes $95,001, then they won’t get that discount and they’d be paying the full premium, so in my example $1200 x 12 = $14,400 annually, which translates into $5375 more annually if you make $1 more.

I’m not sure where they came up with that magic number of $9035 but it’s really not that far off if you start looking at richer benefit plans!

Filed under: 90 day waiting period, HR, National Healthcare, Reform | Tags: 90 day waiting period, Reform, Waiting period

On March 18, 2013, the Departments of Labor, Treasury, and Health and Human Services issued proposed guidance regarding eliminating waiting periods in excess of 90 days for employees who are eligible for their company’s health insurance plan. A waiting period is defined as the time that must pass before an employee can be covered under a plan. This guidance is effective January 1, 2014, and remains in effect at least through December 31, 2014.

For plan years beginning on or after January 1, 2014, a waiting period for employees and dependents who are otherwise eligible for coverage under an employer’s group health plan cannot be longer than 90 calendar days, including weekends and holidays. Plans will no longer be able to use a “three month” waiting period as it might exceed 90 calendar days. This also means that employers can no longer use a waiting period in which coverage begins the first of the month following 90 days of service.

The proposed regulations also clarify how this provision applies to variable-hour employees where plan eligibility is based upon a specified number of hours worked. A plan is considered in compliance with the waiting period requirement if the hours of service required for eligibility for coverage under the plan do not exceed 1,200 hours. Note: This requirement cannot be re-applied to the same individual each year.

Filed under: HR

We all know how hard it is in this economy to keep the good employees we have and attract the good ones we want. How much do the “bells and whistles” we offer as an employer weigh in on the choice employees make to stay with us or move on; or new employees to find a new home within our firm?

Kyle Lagunas, an HR Market Analyst at Software Advice, takes a look at just this, in his blog “Software Advice”. Sometimes it is just the “little things” that make the big difference.

Click here to read more.