Filed under: Combs & Company Blog, Insurance 101, New York PFL, Paid Family Leave, PFL, Susan L Combs | Tags: Combs & Company, Insurance Terms, New York Paid Family Leave, PFL, Susan L Combs

We have been getting a lot of questions on this so thought I’d give you a breakdown of how it works and what to expect for January 1, 2018 with New York Paid Family Leave.

We have been getting a lot of questions on this so thought I’d give you a breakdown of how it works and what to expect for January 1, 2018 with New York Paid Family Leave.

What is it?

As of January 1, 2018, most employees who work in New York State will be eligible for Paid Family Leave. This is leave not for yourself, this is leave to take care of others which include: spouse, domestic partner, child, stepchild, parent, stepparent, in-laws, grandparent or grandchild. This is also available due to Active Military Duty Deployment. They are not including siblings at this time, so keep that in mind.

Who is eligible?

- Full-time employees: If you work a regular work schedule of 20 or more hours per week, you are eligible after 26 consecutive weeks of employment.*

- Part-time employees: If you work a regular work schedule of less than 20 hours per week, you are eligible after working 175 days, which do not need to be consecutive.*

- You are eligible regardless of your citizenship and/or immigration status.

*These weekly counts look back at 2017. What this means is if you have been a full-time employee for 2017 and been working over 20 hours per week for the 26 weeks leading up to January 1, 2018 – you would be eligible to go out on claim January 1, 2018.

How much is taken out of my paycheck?

- This is a prorated amount (no more than $1.65 per week) depending on how the company does payroll, but it is basically capped around $85 FOR THE YEAR, so you won’t even notice it coming out of your check! Here is the deductions calculator if you want to know exactly!

How much do I get?

- This is going to be a 4-year phase in and you are going to start seeing these acronyms a lot: AWW and SAWW. AWW stands for Average Weekly Wage and SAWW stands for State Average Weekly Wage. The SAWW they are using for 2018 is $1305.92, which translates into the Max Weekly Benefit you can get is $652.96 for 8 weeks.

- Here is a grid showing the phase in numbers from state website!

Benefits Increase Through 2021

| Year | Weeks of Leave | Benefit |

| 2018 | 8 weeks | 50% of employee’s AWW, up to 50% of SAWW |

| 2019 | 10 weeks | 55% of employee’s AWW, up to 55% of SAWW |

| 2020 | 10 weeks | 60% of employee’s AWW, up to 60% of SAWW |

| 2021 | 12 weeks | 67% of employee’s AWW, up to 67% of SAWW |

- Example: An employee who makes $1,000 a week would receive a benefit of $500 a week (50% of $1,000). Another employee who makes $2,000 a week would receive a benefit of $652.96, because this employee is capped at one-half of New York State’s Average Weekly Wage —currently $1,305.92. Half of that amount is $652.96.

- Leave can be taken either all at once or in full-day increments. You may take the maximum time-off benefit in any given 52-week period. The 52-week clock starts on the first day you take Paid Family Leave.

As an Employee, what do you need to do if you need to go out on claim?

- Notify your employer. You need to do this at least 30 days before you want your leave to start (if possible). For example, if you are due with a baby 2/1, you can plan ahead, but if the baby comes 4 weeks early, you need to notify your employer as soon as possible.

- Submit a claim form. You’ll need to ask your employer or the employer’s insurance company what forms you should complete and get the supporting documentation that is requested. Make sure to keep a copy for your records. You can actually submit your claim form 30 days before or 30 days after the event and then the carrier has 18 days to respond to your claim.

Click here for the Employee Fact Sheet by New York State!

As an Employer, what do you need to do?

- If you have State Mandated Disability, your carrier will most likely offer the Paid Family Leave coverage. If you haven’t received an email or a letter from your carrier, you need to reach out to them ASAP.

- As this is an Employee Paid benefit, Employees will have deductions taken out of their paychecks for this. If your payroll company hasn’t reached out to you about this, check with them before your first January 2018 payroll run.

- You also must Post a Workforce Notice, which you should also be getting in the mail from your carrier.

- If you currently Self Insure your Disability, here’s a list of carriers that you can get this coverage from!

- Update your handbook to include the new policy if you have one!

Click here for the Employer Fact Sheet by New York State!

I know this doesn’t cover absolutely everything you might have a question on, but if you read and understand this, you’ll be more equipped than 99% of New Yorkers out there!

Filed under: Combs & Company, Combs & Company Blog, Insurance 101, Susan L Combs, Uncategorized | Tags: Combs & Company Vlog, EPOs, Exclusive Provider Organizations, Insurance 101, Insurance Terms, Susan L Combs

Check our our quick video about Exclusive Provider Organizations (EPOs)!

For more Insurance 101, check our our Combs & Co YouTube Channel!

Filed under: Combs & Company, Insurance 101, Vlog | Tags: Beneficiary, Combs & Company, Health Insurance 101, Insurance Terms, Susan L Combs

Check out our quick video on Who is a Beneficiary!

More videos where this came from… Check out the Combs & Co YouTube channel for more!

Filed under: Affordable Care Act, Combs & Company, Combs & Company Blog, HR, Important Notice, Obamacare, Reform, Susan L Combs | Tags: ACA, Combs & Company, Insurance Terms, National Healthcare, Penalties

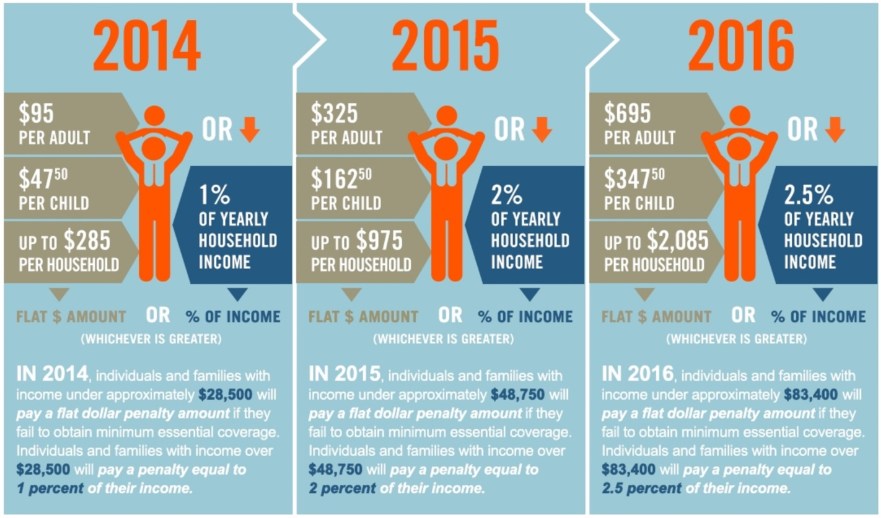

So we are in the home stretch! Three more days to go and then Open Enrollment ends for 2016. From experience, I have learned that many people wait until the last minute to pick a plan and some people just continue to bury their heads in the sand. So for those of you that are wondering, how much it’s going to cost you if you don’t get your act together, take a look at this user friendly graphic that will show you what to expect!

Filed under: Affordable Care Act, Combs & Company, Combs & Company Blog, Obamacare, PPACA, Reform | Tags: ACA, Combs & Company, Insurance Terms

WHO? . . . ALEs must report.

For 2015 information reporting requirements, an Applicable Large Employer (ALE) is subject to the Affordable Care Act health coverage information reporting requirements. For more information on Employer Shared Responsibility and which employers are required to offer coverage, contact our office.

Please note that this applies to:

• Employers who had 50 or more full-time employees, including full-time equivalent employees, in 2014

• Governmental, tribal, tax-exempt, or for-profit employers

• ALEs-whether or not the employers offered health coverage to employees

WHAT? . . . IRS reporting is required for health coverage information.

An ALE must file information returns with the IRS and provide statements to each employee who was a full-time employee for at least one month of the year about health coverage. The employer is required to indicate if they offered health coverage or did not offer health coverage.

WHICH FORMS? . . . Forms 1094-C and 1095-C must be submitted to the IRS.

• Form 1094-C. Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Return is used to report to the IRS summary information for each employer and to transmit Form 1095-C to the IRS.

• Form 1095-C. Employer-Provided Health Insurance Offer and Coverage, is used to report required information to your employees and to report information about each employee to the IRS.

WHEN? . . . Prepare now for the upcoming due dates.

• Forms 1095-C must be provided to your employees by March 31, 2016.

• Forms 1094-C and 1095-C are due to the IRS by May 31, 2016, if filing by paper, or June 30, 2016, if filing electronically.

NEED HELP?

Contact us immediately for a solution that fits your unique filing needs.

Filed under: Administrative Fix, Affordable Care Act, NAHU, National Healthcare, Obamacare, PPACA, Reform | Tags: 1094, 1095, 6055, 6056, ACA, Employer Requirment, Insurance Terms, NAHU, National Healthcare

This morning, the Internal Revenue Service (IRS) made an announcement that may affect your clients regarding compliance to new Affordable Care Act (ACA) mandated coverage reports (6055 and 6056) for 2015. The IRS announced that it is giving employers additional time to file certain reports. In Notice 2016-4, the IRS stated that it is delaying filing deadlines after determining that “additional time to adapt and implement systems to gather, analyze, and report this information” was needed by employers, insurers, and other providers.

This morning, the Internal Revenue Service (IRS) made an announcement that may affect your clients regarding compliance to new Affordable Care Act (ACA) mandated coverage reports (6055 and 6056) for 2015. The IRS announced that it is giving employers additional time to file certain reports. In Notice 2016-4, the IRS stated that it is delaying filing deadlines after determining that “additional time to adapt and implement systems to gather, analyze, and report this information” was needed by employers, insurers, and other providers.

The deadline for employers to electronically file 1094 forms for 2015 was extended by three months from March 31, 2016, to June 30, 2016. The deadline for filing by paper was also extended by three months from February 29, 2016, to May 31, 2016. Additionally, the deadline for providing employees with 1095 forms for 2015 was extended from February 1, 2016, to March 31, 2016.

Click here for today’s IRS announcement or for background about the mandated ACA coverage reports.

Filed under: Health Insurance | Tags: Copay, Deductible, Health Insurance 101, How does a deductible work, Insurance Glossary, Insurance Terms, Out of Network, Summary of Benefits & Coverage

So many times we are asked to explain health insurance terms to our clients and their employees. Thought we would share the most commonly used terms and explain how it works!

Health Insurance Glossary

Prescription Drugs:

Drugs come in 3 tiers, below are the details:

A tiered formulary offers its lowest copay for generic drugs (Tier 1), charges you a little more for brand-name drugs (Tier 2) still under patent (that is, you have no option but to take them if you need them) and a lot more for what formularies call “non-preferred” drugs or non-formulary brand named drugs (Tier 3) most often, they are brand-name drugs you choose to purchase in spite of available generics), and new drugs whose cost is higher than alternative therapies (though these may eventually become tier two drugs).

Deductible: The deductible is the amount an individual must pay for health care expenses before insurance (or a self-insured company) covers the costs. Often, insurance plans are based on yearly deductible amounts. For Prescription Drugs, you have a one-time annual Deductible that has to be satisfied for Tier 2 and Tier 3 Drugs only.

Major Medical In Network:

Deductible: The deductible is the amount an individual must pay for health care expenses before insurance (or a self-insured company) covers the costs. Often, insurance plans are based on yearly deductible amounts.

Coinsurance: refers to money that an individual is required to pay for services, after a deductible has been paid. By definition it is the split between the Insurance Company and the Insured. Coinsurance is always specified by a percentage. For example, the employee pays 20 percent toward the charges for a service and the insurance company pays 80 percent.

Out-of-Pocket Maximum: The dollar amount of claims filed for eligible expenses at which point you’ve paid 100 percent of your out-of-pocket and the insurance begins to pay at 100 percent. Stop-loss is reached when an insured individual has paid the deductible and reached the out-of-pocket maximum amount of co-insurance.

Copayment: is a predetermined (flat) fee that an individual pays for health care services, in addition to what the insurance covers. For example, some plans require a $30 copayment for each office visit, regardless of the type or level of services provided during the visit.

DXL: Stands for – Diagnostic X-ray and Lab, when you see this, it will give you the amount of the copayment associated with these services.

Lab Fees: The copayment associated with lab fees.

Hospital Benefits In Network:

Hospital In-Patient: Copay associated with hospitalizations where you are admitted for overnight stays.

Hospital Out-Patient: Copay associated with hospitalizations where you are admitted, but you do not have an overnight stay.

Emergency Room: Copay associated with Emergency Room visit, this is waived if you end up being admitted.

Surgical Benefits In Network:

Surgical In-Patient: Copay associated with an in hospital surgical procedure where you are going to be admitted for an overnight stay.

Surgical Out-Patient: Copay associated with an in hospital surgical procedure where you are admitted, but you do not have an overnight stay.

Mental Health & Substance Abuse In Network:

Mental Nervous In-Patient: Copay associated when admitted to a facility for overnight stays.

Substance Abuse In-Patient: Copay associated when admitted to a facility for overnight stays, aka rehab.

Mental Nervous Out-Patient: Copay associated with visit aka therapist visit

Substance Abuse Out-Patient: Copay associated with visit aka Out Patient Program

Out of Network Services:

All Out of Network are treated the same, the deductible has to be satisfied first, then a percentage of the Allowable Charges are covered until an Out of Pocket Maximum is reached, then 100% of the Allowable Charges are covered. Keep in mind, if you go to an Out of Network Doctor that charges over the Allowable Charge Amount, then you will be balance billed.