Filed under: Combs & Company Blog, Health Insurance, Insurance 101, PPACA, Reform | Tags: Combs & Company Vlog, Employer Responsibility, Insurance 101

Check our our quick video about Employer Responsibility!

For more Insurance 101, check our our Combs & Co YouTube Channel!

Filed under: Affordable Care Act, Combs & Company, Combs & Company Blog, HR, Important Notice, Obamacare, Reform, Susan L Combs | Tags: ACA, Combs & Company, Insurance Terms, National Healthcare, Penalties

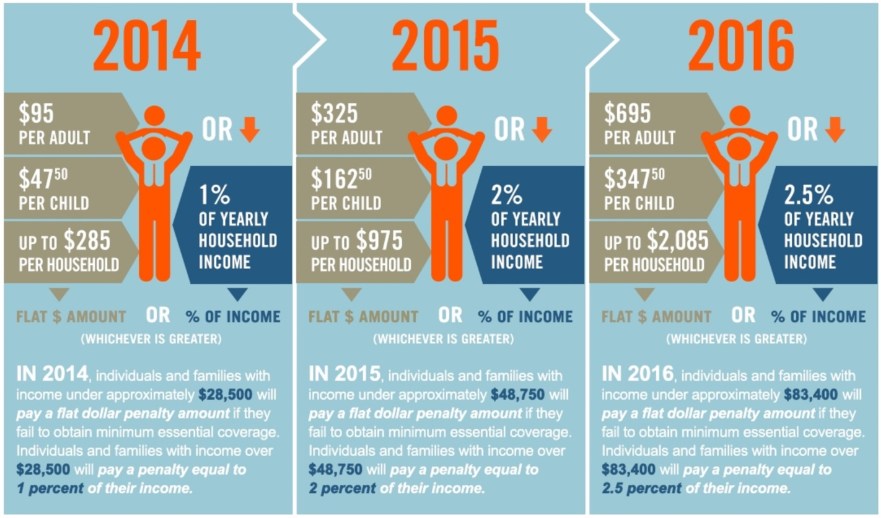

So we are in the home stretch! Three more days to go and then Open Enrollment ends for 2016. From experience, I have learned that many people wait until the last minute to pick a plan and some people just continue to bury their heads in the sand. So for those of you that are wondering, how much it’s going to cost you if you don’t get your act together, take a look at this user friendly graphic that will show you what to expect!

Filed under: Affordable Care Act, Combs & Company, Combs & Company Blog, Obamacare, PPACA, Reform | Tags: ACA, Combs & Company, Insurance Terms

WHO? . . . ALEs must report.

For 2015 information reporting requirements, an Applicable Large Employer (ALE) is subject to the Affordable Care Act health coverage information reporting requirements. For more information on Employer Shared Responsibility and which employers are required to offer coverage, contact our office.

Please note that this applies to:

• Employers who had 50 or more full-time employees, including full-time equivalent employees, in 2014

• Governmental, tribal, tax-exempt, or for-profit employers

• ALEs-whether or not the employers offered health coverage to employees

WHAT? . . . IRS reporting is required for health coverage information.

An ALE must file information returns with the IRS and provide statements to each employee who was a full-time employee for at least one month of the year about health coverage. The employer is required to indicate if they offered health coverage or did not offer health coverage.

WHICH FORMS? . . . Forms 1094-C and 1095-C must be submitted to the IRS.

• Form 1094-C. Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Return is used to report to the IRS summary information for each employer and to transmit Form 1095-C to the IRS.

• Form 1095-C. Employer-Provided Health Insurance Offer and Coverage, is used to report required information to your employees and to report information about each employee to the IRS.

WHEN? . . . Prepare now for the upcoming due dates.

• Forms 1095-C must be provided to your employees by March 31, 2016.

• Forms 1094-C and 1095-C are due to the IRS by May 31, 2016, if filing by paper, or June 30, 2016, if filing electronically.

NEED HELP?

Contact us immediately for a solution that fits your unique filing needs.

Filed under: Administrative Fix, Affordable Care Act, NAHU, National Healthcare, Obamacare, PPACA, Reform | Tags: 1094, 1095, 6055, 6056, ACA, Employer Requirment, Insurance Terms, NAHU, National Healthcare

This morning, the Internal Revenue Service (IRS) made an announcement that may affect your clients regarding compliance to new Affordable Care Act (ACA) mandated coverage reports (6055 and 6056) for 2015. The IRS announced that it is giving employers additional time to file certain reports. In Notice 2016-4, the IRS stated that it is delaying filing deadlines after determining that “additional time to adapt and implement systems to gather, analyze, and report this information” was needed by employers, insurers, and other providers.

This morning, the Internal Revenue Service (IRS) made an announcement that may affect your clients regarding compliance to new Affordable Care Act (ACA) mandated coverage reports (6055 and 6056) for 2015. The IRS announced that it is giving employers additional time to file certain reports. In Notice 2016-4, the IRS stated that it is delaying filing deadlines after determining that “additional time to adapt and implement systems to gather, analyze, and report this information” was needed by employers, insurers, and other providers.

The deadline for employers to electronically file 1094 forms for 2015 was extended by three months from March 31, 2016, to June 30, 2016. The deadline for filing by paper was also extended by three months from February 29, 2016, to May 31, 2016. Additionally, the deadline for providing employees with 1095 forms for 2015 was extended from February 1, 2016, to March 31, 2016.

Click here for today’s IRS announcement or for background about the mandated ACA coverage reports.

Filed under: Affordable Care Act, Health Insurance, HR, Obamacare, PPACA, Reform | Tags: ACA Auditing Services, Insurance Consulting

Since the start of 2014 we’ve been approached by CPAs, attorneys, and other trusted advisors to assist them with Affordable Care Act (ACA) audits, to determine if their clients will be subject to the “Pay or Play” provision come 2015, and then in 2016 if they have more than 50 Full-Time Equivalent (FTE) employees. I wanted to take this opportunity to introduce our ACA auditing services to you.

Currently I’m one of seven brokers in the New York Metro area with a Patient Protection & Affordable Care Act (PPACA) certification through the National Association of Health Underwriters (NAHU). The certification is key, as I’m trained on all the variables within the ACA law and how it impacts companies of various sizes; plus the continuing education keeps me fully informed as Washington adjusts different provisions of the law.

For 2015, companies that have more than 100 FTE employees will be required to offer health coverage to all employees or they will be subject to a fine. That coverage must include the 10 Essential Benefits, or the company will be subject to a different fine. Combs & Company will perform the ACA audit and produce a report that highlights all provisions with which a company must comply (and the consequences if they don’t). We’ll also devise a look-back measurement the company should use to minimize any potential penalties. We’ll also review any Common Ownership issues, as these are often overlooked areas that can impact companies.

This is not a pitch to replace a company’s current broker. We’re offering this service to support a company’s current setup and because we know the level of expertise we bring to the table is not yet common in the industry. (Nor do most brokers want to assume the liability.) We will work with your client’s current broker to gather as much information as possible and then incorporate them into the audit process.

Our service is offered at a rate of $250/hour. The length of each audit depends on the complexity of your client’s business and health plans. We also have an in-house ERISA Attorney who can provide additional services for a flat fee, should any compliance issues come to light during the ACA audit.

If you’re interested in finding out more or having your client schedule a planning meeting with us, feel free to reach out!

Filed under: Affordable Care Act, Health Insurance, Important Notice, National Healthcare, Obamacare, PPACA, Reform

You’d be amazed at how many phone calls and emails we have been getting about signing up for the exchange after the deadline. Unfortunately….people that have waited are not special. Everyone had an Open Enrollment Period began October 1st and officially ended in the state of NY as of March 31st, that was 6 months….no one can say they didn’t have enough time but still so many people chose to bury their head in the sand. So if you are one of these people that didn’t sign up what does this actually mean to you:

You’d be amazed at how many phone calls and emails we have been getting about signing up for the exchange after the deadline. Unfortunately….people that have waited are not special. Everyone had an Open Enrollment Period began October 1st and officially ended in the state of NY as of March 31st, that was 6 months….no one can say they didn’t have enough time but still so many people chose to bury their head in the sand. So if you are one of these people that didn’t sign up what does this actually mean to you:

- If you had started an enrollment on the New York State of Health Exchange Marketplace (https://nystateofhealth.ny.gov/) you have until April 15th to get your act together and get your application completed.

- If you haven’t started an application yet and you are CURRENTLY UNINSURED, then you are out of luck with Exchange and other Private options until the next Open Enrollment which is set to begin on 11/15/14 for an enrollment of January 1st, 2015. Sorry, no one’s special here.

- If you are CURRENTLY INSURED you will be able to take coverage with the Exchange or other private insurance for effective dates after 4/1 as long as you can prove that you have had a Qualifying Life Event. These are listed below:

- Individual or dependent loses minimum essential coverage due to:

- job loss

- divorce

- death of a spouse

- becoming ineligible for Medicaid or Child Health Plus

- expiration of COBRA

- health plan is decertified

- Marriage, birth, adoption, or placement for adoption

- Gaining status as a citizen, national, or lawfully present individual

- Consumer is newly eligible or ineligible for tax credits and/or cost sharing reductions

- Permanent move to an area that has different health plan options

- Marketplace staff or contractor enrollment error

- Qualified Health Plan violated a provision of its contract

- American Indians can enroll or change plans one time per month throughout the year

- Individual or dependent loses minimum essential coverage due to:

Not considered a Qualifying Life Event:

- Voluntarily dropping other health coverage

- Being terminated for not paying your premiums

- Losing coverage that is not minimum essential coverage, in accordance with HHS guidelines

Moral of the story: Be more proactive next year!!!

Filed under: Affordable Care Act, Exciting News, Health Insurance, HR, Important Notice, National Healthcare, Obamacare, PPACA, Reform

A question that comes up time and time again with the Affordable Care Act is: “How does the Individual Responsibility (aka Mandate) Penalty work?”

To avoid the penalty you must enroll in a marketplace plan OR have private coverage no later than March 31st, 2014. If you do not, below are a breakdown of the penalties you will face.

- 2014: Greater of $95 per adult and $47.50 per child under age 18 or 1% of household income

- 2015: Greater of $325 per adult and $162.50 per child under age 18 or 2%

- 2016: Greater of $695 per adult and $347.50 per child under age 18 or 2.5% of taxable gross income capped at the average bronze-level insurance premium (60% actuarial) rate for the person’s family.

**The total family penalty is capped at 300% of any annual flat dollar amount for those 18 and over.

**If the penalty applies for less than a full calendar year, the penalty will be 1/12 of the annual amount per month without coverage.

Example:

Let’s look at the O’Brien family of 4 that has 2 children under the age of 18 and the family household income is $100,000 per year.

Just to make the example easier, we are giving everyone names….Meet the O’Brien Family: Mom – Samantha; Father – Mark; Son – Luke; Daughter – Sarah

Upfront we know that the Max Penalty the O’Brien’s’ can be given is: $570 (this is figured by a $95 penalty each for Samantha & Mark since they are the only ones over 18 x 300%), now let’s look at the breakdown if they would hit the Max Penalty….

Remember, it is the GREATER of the below up to the Max Penalty:

Flat dollar amount penalty calculation : $95 (Samantha) + $95 (Mark) + $47.50 (Luke) + $47.50 (Sarah) = $285

Percentage amount penalty calculation: 1% of $100,000 = $1000

Results: Since the Max Penalty the O’Brien family can be given in this example is $570, this will be the penalty they will be responsible for, since the 1% of household income exceeds this amount. This amount will be tacked on when Samantha and Mark’s taxes are calculated at the end of the year, so if they were planning on a nice refund this year, that will be deducted from that refund. Keep in mind that if the O’Brien’s do not pay taxes, as of now, there is no mechanism to collect this penalty.

Filed under: Administrative Fix, Affordable Care Act, Health Insurance, Important Notice, Obamacare, PPACA, Reform

As many have heard, Obama has offered a “fix” to many of the people that have gotten notifications of their insurance being canceled. I believe that this report, gives a good picture of it and I want to point out a few things before people start popping the cork and celebrating:

- Obama said that carriers “could” offer the plan for 1 more year…

- Obama pushed the ultimate decision over to the States and the Carriers…so far California, Idaho, Virginia and Kentucky have said no to this fix.

- If the carrier choose to offer to extend, then they are going to have to send the customers a comparison that shows the differences between their plan and all the Exchange Plans that they are offering, what this translates to is more work when we are already 45 days out, and the carriers do not have the extra time on their hands right now.

- The carriers do not have an actuarial value of any of these plans since they are not in their plan offerings and I believe that this would result in even higher prices as they would have to put in more man hours to reincorporate these plans.

If you have gotten a cancelation notice, I encourage you to call your carrier and see if they are going to pony up and continue to offer your plan, but don’t be shocked if you end up being one of many that they tell no.

Filed under: Employer Requirement, Health Insurance, Important Notice, National Healthcare, Reform

Pretty much all employers will need to provide their employees with written notice that includes information regarding the Exchange (now called the Health Insurance Marketplace). The deadline to provide the notice is fast approaching; the notice must be provided to each employee not later than October 1, 2013. Regardless of the size of your company and even if you currently do not offer coverage to your employees you *SHOULD* send this information out. The reason we say should instead of MUST is because as of last week, this has been another penalty that has been delayed and they haven’t told us when it will come back. Originally it was speculated a $100 fine for every day you have not complied with the request. We still encourage everyone to comply now as then when / if the penalty goes into effect you are all in compliance.

Click below to view the English version of the notices that you can provide to your employees:

English notice if you DO offer coverage

English notice if you DO NOT offer coverage

I had a client that sent me this article and then asked if it was true, that if someone makes $1 more that the family would be paying $9,355 more annually.

I had a client that sent me this article and then asked if it was true, that if someone makes $1 more that the family would be paying $9,355 more annually.

I know there are a lot of confusing articles out there right now and this was written with a shock factor to get you to read the article, and for my client….it worked! He read it, and he contacted me to be his “BS Meter” as he put it.

Here is an example to further explain why this article is saying what it is say:

Ok, so let’s say it is a family of 4.

400% of the federal poverty level is around $95,000 for a family of four in 2014. If they are making $95,000, then with their subsidy aka discount they will get in the Exchange / Marketplace they cannot spend more than 9.5% of $95,000 on healthcare. Which translates to $9025 annually = $752 per month (just as a barometer, most family coverage in NY starts at around $1200 per month for a very watered down plan).

If the person makes $95,001, then they won’t get that discount and they’d be paying the full premium, so in my example $1200 x 12 = $14,400 annually, which translates into $5375 more annually if you make $1 more.

I’m not sure where they came up with that magic number of $9035 but it’s really not that far off if you start looking at richer benefit plans!